100 days is probably not the way to measure the organizational effectiveness of the new head of this institution, according to huge tasks facing the Accounting Chamber (the ACU). At the same time, I believe that this time is enough to assess the current situation within the institution, identify the areas where maximum efforts should be concentrated, respond to urgent challenges, and develop strategic plans for the future.

Before listing the main achievements of the start-up period, it is worth to note that at the beginning of 2024, the institution had a sufficient basis for large-scale changes primarily due to long-term cooperation with international technical support projects, such as "Strengthening Capacities in External Audit in Line with International Standards (EU4ACU)". Our partners did not stop supporting the institution, but only strengthened it from year to year: this includes assistance in drafting internal methodological document, and continuous improving the auditors' skills, and consulting support in planning and conducting audits in accordance with international standards. Due to this, we had a good "launch pad" for fundamental changes, the results of which, I am confident, will be visible by the end of this year. Of course, all the results obtained are the achievements of the ACU Team and collaboration with international partners.

We started with an in-depth analysis of all processes within the institution and identified a number of critical weaknesses required an urgent response. Below is a detailed description of the individual steps.

One of the biggest challenges in our work is rapid institutional reforming. Last year, the Verkhovna Rada of Ukraine registered a new bill on the ACU. Now it is considered by the parliamentary committees. Simultaneously, a Working group including representatives of the ACU gathers and drafts another bill. However, the issue of time is important for our institution, while legislative work can take much time.

I should remark that the ACU is not a subject of legislative initiative. Thus, we could provide comments or suggestions and express our position on certain issues. The first significant outcome is taking into account by the MPs our position regarding urgent amendments to relevant legislation to bring the Accounting Chamber’s powers on auditing into full compliance with international standards. Thus, Law of Ukraine No. 3621-IX (dated March 21, 2024) amended articles 4, 7 and 35 of the Law of Ukraine “On the Accounting Chamber”, which regulate the issues of compliance audits conducted by the Accounting Chamber.

Compliance audit is one of three types of audits carried out by Supreme Audit Institutions. Compliance audits are aimed at evaluating an organization’s adherence to legislation or breach of legal requirements to take possible corrective actions and prevent such discrepancies in the future. Compliance audit plays an important role in ensuring compliance with the principles of transparency, accountability and good governance in the public sector.

This type of audit was not provided among the public external financial control (audit) measures in the current Law of Ukraine “On the Accounting Chamber”. Only some elements of the compliance audit were distributed between financial and performance audits. At the same time, according to the International Standards of Supreme Audit Institutions (ISSAI), the methodology of this audit provides for special requirements on planning, procedures for obtaining audit evidence, as well as a special report structure.

Consequently, these changes of the legislation allows the Accounting Chamber applies the Compliance Audit Methodology, approved by the Decision of the Accounting Chamber in 2023, to plan and conduct compliance audits on an equal basis with all other Supreme Audit Institutions in the world.

Another fundamental decision is the Accounting Chamber will conduct all audits according to INTOSAI standards since 2024.

In general, the implementation of the main principles of the International Organization of Supreme Audit Institutions (INTOSAI) and the INTOSAI System of Professional Documents (IFPP) in the activities of the Accounting Chamber and development of the ACU documents based on them, are inseparably connected with the process of fulfilling the obligations defined by the Association Agreement between Ukraine and the EU (Article 347) and other measures taken to fulfill such obligations.

Professional standards and guidelines are extremely important for the quality and effectiveness of audits, and their application ensures an increased confidence of auditee and stakeholders in their results.

The current Law, adopted in 2015, allows the Accounting Chamber to implement international standards and methodologies in its work. However, this opportunity has been used poorly and unsystematically, since then. The audits that were conducted according to these standards could be counted on the fingers of one hand.

At the same time, it was necessary to ensure a high-quality translation of standards and guidelines of the INTOSAI System of Professional Documents into the state language to refer to them. For this purpose, the Accounting Chamber contributed to the translation of ISSAI 100 "Fundamental Principles of Public Sector Audit" into Ukrainian. The Accounting Chamber approved by decision this Ukrainian translation of standard to work.

I will remind that the official languages of INTOSAI are Arabic, English, French, German and Spanish. Translation of ISSAI 100 into Ukrainian will allow the Accounting Chamber to prepare documents in a better quality, and will give external users to understand their content better.

It is also about providing effective and specific recommendations based on the results of audits.

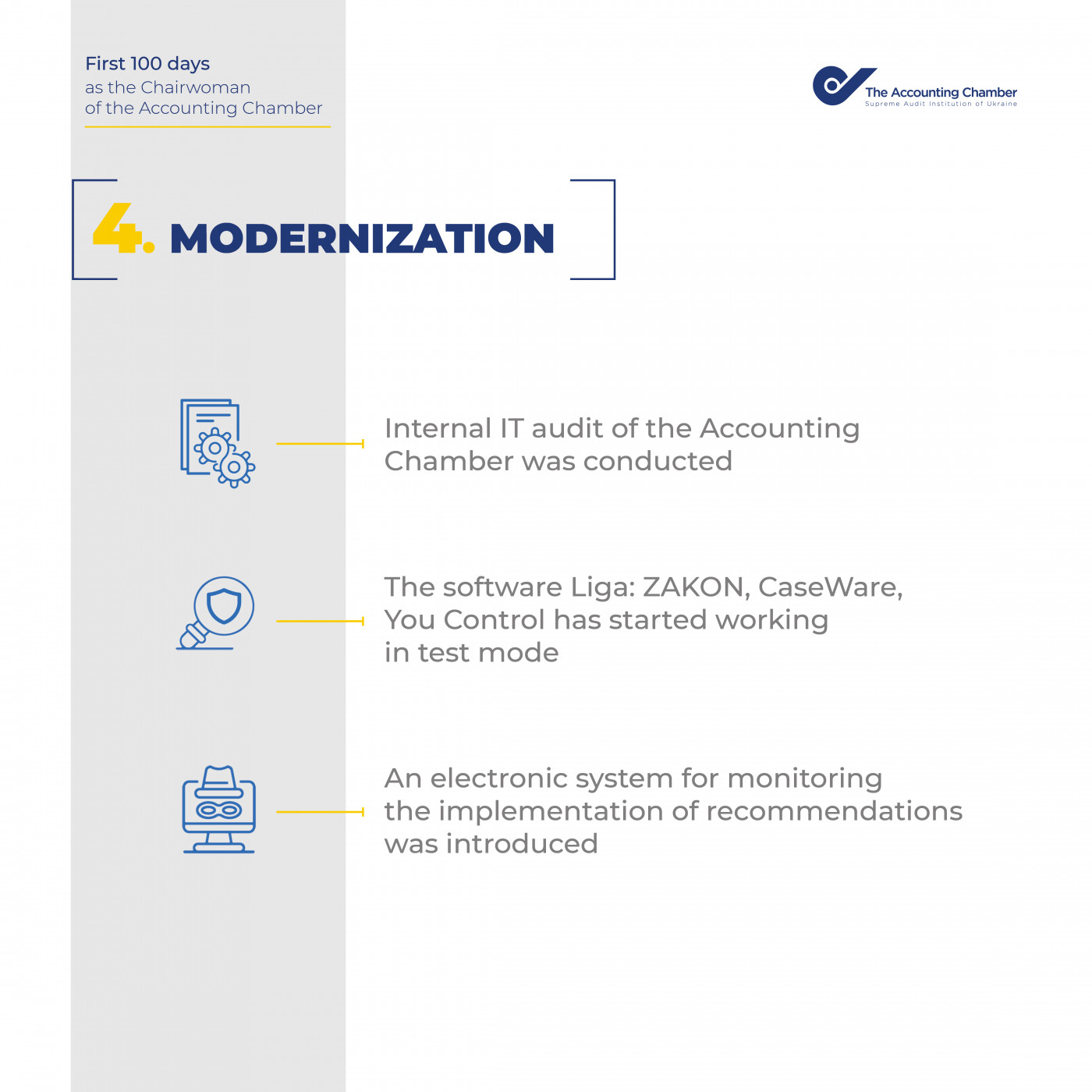

By the way, we have collected all the information on the status of each recommendation provided by the Accounting Chamber from 2018 to 2023. Unfortunately, the statistics are disappointing: over six years, out of 4,802 recommendations, only 2,562 have been fully implemented, 779 have been partially implemented, and another 370 are in the process of being implemented. In addition, 141 recommendations of the Accounting Chamber have completely lost their relevance.

During this analysis, another problem was identified: there is no common standard regarding the form of recommendations; they sometimes look radically different from report to report. For example, in one report there may be more than a hundred of them, in another - only three, in one they are described very widely and specifically, in another - only in short general phrases.

Currently, together with the EU4ACU project, we are implementing an internal digital system for monitoring of recommendations implementation. This tool will allow us to instantly receive data on the status of any audit recommendations, generate analytics based on them, and then improve control over compliance with deadlines.

I would like to note that the Action Plan for the implementation of recommendations of the European Commission, presented in the Report on Ukraine’s progress within the framework of the European Union Enlargement Package 2023 (clause 48 of section 32 “Financial control”) envisage that the Accounting Chamber improves the system of monitoring recommendations and informing stakeholders (government bodies, civil society institutions, political parties, territorial communities, etc.) about its results for an appropriate response.

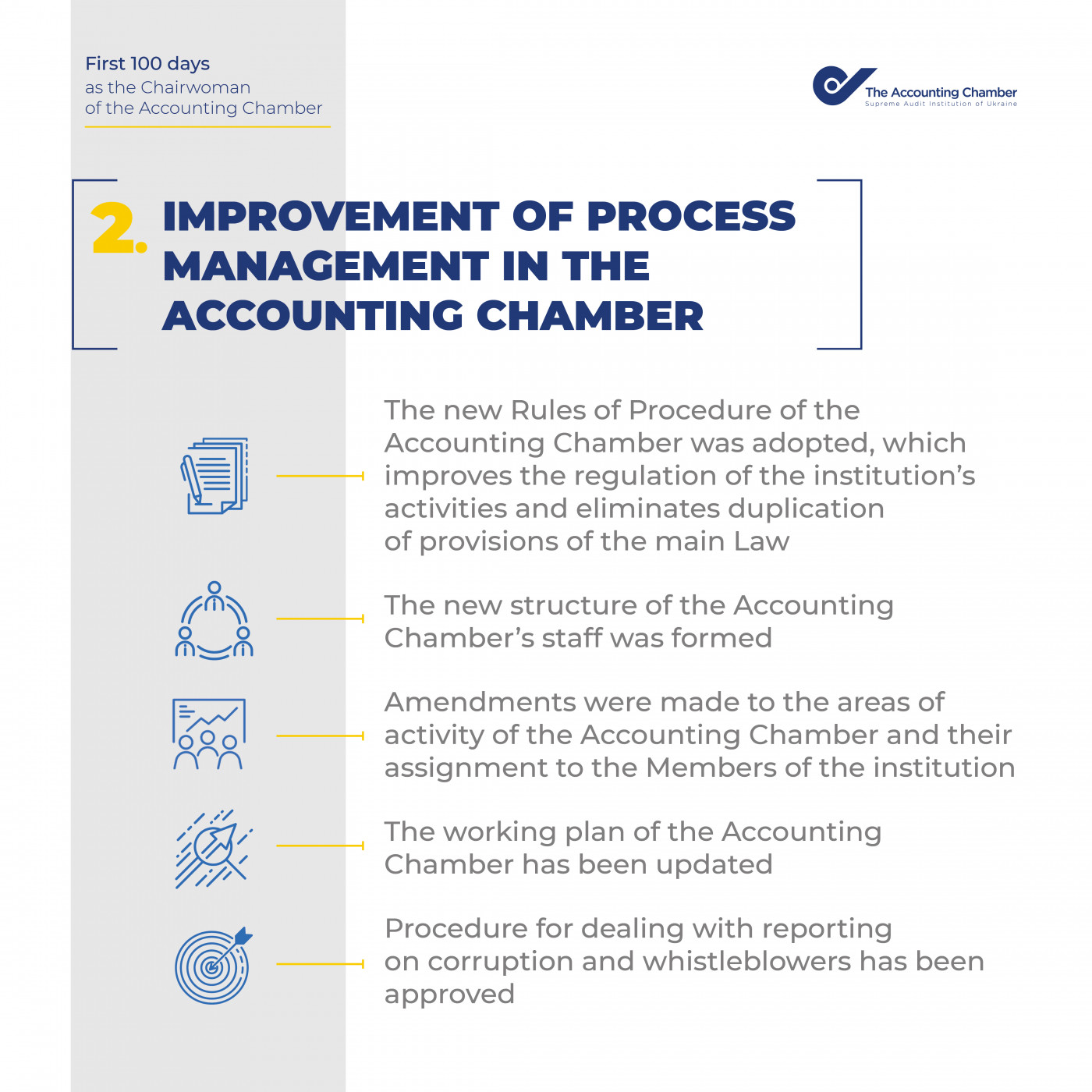

As for our "inner workings" - here we managed to do even more than we had hoped at first. Such decisions as a change of activity areas distribution principles of the Accounting Chamber, a new Regulation or a new structure of the apparatus are adopted exclusively collegial. Therefore, the debate on these issues could have lasted for a long time, but thanks to the constructive position of colleagues, this did not happen.

Probably the key decisions is to change the approaches to determining the activity areas of the Accounting Chamber and assigning them to Members of the institution. The change of areas and their rotation between Members is not a new action (previously this could happen several times a year). We did not just accept the area of one member of the ACU and transfer it to another. We changed the principle of determining areas, forming them according to the functional classification of expenses and budget lending. Previously, such distribution between Members of the ACU was done by assigning to them specific of control objects, which did not always concern only one function of the state. That is, one Member of the ACU could be responsible for several varied and unrelated functions, such as anti-corruption activities and culture. In this case, one function could be distributed among several Members of the ACU. This distribution principle did not allow audits to be conducted qualitatively and without internal contradictions, covering the state of affairs in the entire sphere (for example, in law enforcement), did not contribute to a comprehensive assessment of the problem, and did not lead to the formation of recommendations for truly effective ways to solve them.

The necessity of adopting a new Regulation of the ACU is explained by the outdated and sometimes contradictory content of the previous document. The new Regulation is a clear, logical, and well-structured document formed in compliance with all principles of legality. It ensures the avoidance of duplications of the Law's norms, updates the specifics of implementing certain powers of the ACU, and improves the regulation of its activities.

The restructuring of the institution's apparatus also aims to optimize the distribution of human resources to ensure the completion of all tasks facing the institution, take into account changes regarding the definition and distribution of directions, and strengthen weaknesses in the structure, among other goals.

Additionally, there is currently the ongoing technical modernization of the institution. We are working on improving the remuneration system for specialists of certain levels since, due to several miscalculations in the past, people are currently receiving salaries that do not correspond to their workload and qualifications.

Summarizing the aforementioned, I would like to highlight several steps for the near future.

Firstly, we implement the point of the Action Plan for the recommendations execution of the European Commission, mentioned above and prepare proposals for the mechanism introduction for the Verkhovna Rada of Ukraine committees to review all audit reports of the ACU and to undertake parliamentary control measures to increase the level of implementation of the ACU's recommendations (point 48 of chapter 32 "Financial Control"). This remark has significant grounds because, according to the results of our internal analysis, in the past six years, only about a third of all reports of the ACU were considered by the committees of the Verkhovna Rada. The worst indicator was recorded in 2020 when only 9 out of 53 reports sent by the ACU were considered by the relevant committees.

Another important task is to improve the ACU cooperation with law enforcement agencies. This issue concerns the process of providing information to law enforcement officers and subsequent monitoring of criminal proceedings initiated based on this information. Currently, we only record the facts of opening cases, but we do not know which of these cases result in actual convictions.

Furthermore, we plan to implement systematic monitoring of the knowledge level of the ACU auditors and, based on this data, improve the system of planning their internships, training, or qualification enhancement. Currently, such an approach is absent in the institution.

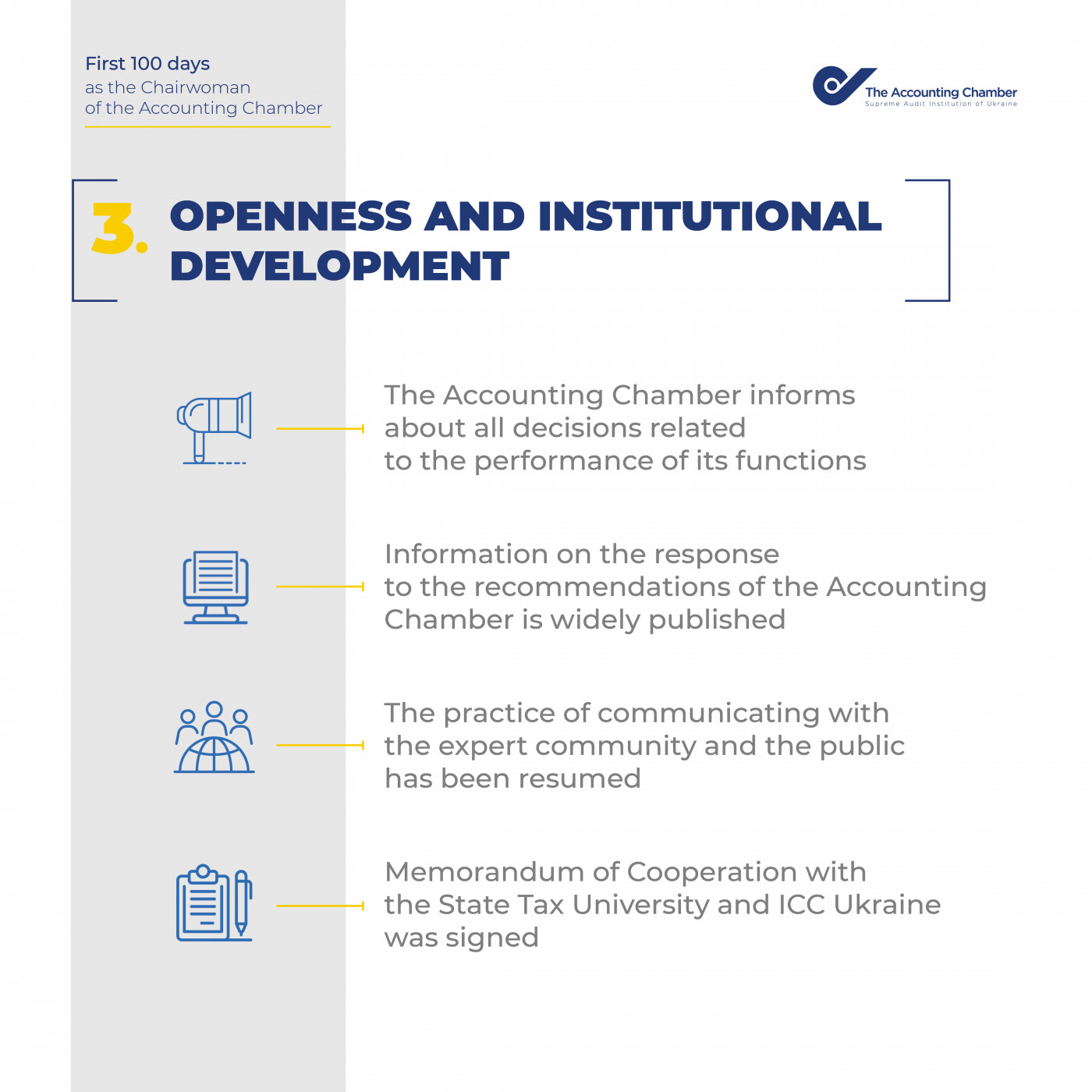

And indeed, we will continue to engage in dialogue with the expert community, civil society institutions, educational institutions to build solid support for the ACU through the exchange of ideas and experiences. By the way, based on these contacts, we will have the opportunity to revive the functioning of the Advisory Scientific Council of the ACU, which has long ceased to exist, although it had significant potential to strengthen the institution's capacity.

Thank you to my colleagues for their position, professionalism, and dedicated work!

To be continued...

OlhaPishchanska, ChairwomanoftheAccountingChamber